October 2025 proved to be one of the most volatile months of the year as global equity markets oscillated between optimism and caution following the Federal Reserve’s first interest rate cut in September. While investors initially expected the move to spark sustained bullish momentum, inflationary concerns, tariff-fears and soft earnings from key sectors reignited market jitters — particularly across small-cap and tech stocks. Despite this turbulence, StockHero’s stock trading bots once again demonstrated their ability to adapt and deliver strong, risk-adjusted performance across a diverse range of market conditions.

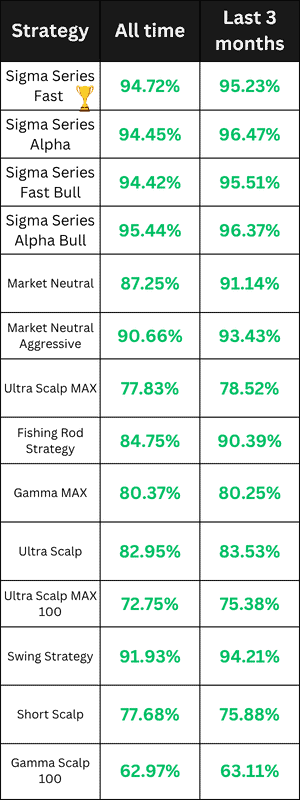

Leading the pack for October was the Sigma Series Alpha, which posted a stellar 96.47% win rate over the last three months and 94.45% all-time performance. Traditionally regarded as a more conservative counterpart to the Sigma Series Fast, the Alpha’s steadier trading logic proved advantageous amid October’s whipsaw market behavior. Its disciplined approach and robust risk management allowed it to outperform even its more aggressive siblings, underscoring the importance of maintaining balanced exposure in uncertain markets.

The Sigma Series Fast continued to perform impressively, with a 95.23% win rate over the past three months. This consistency highlights the strategy’s resilience, especially given that October was a challenging month for momentum-based systems. The Sigma Series Fast Bull and Sigma Series Alpha Bull also maintained high win rates of 95.51% and 96.37%, respectively, showing their continued strength during short-lived bullish phases. Collectively, the Sigma Series remains StockHero’s flagship lineup, proving once again why it forms the backbone of many users’ automated portfolios.

Meanwhile, Market Neutral strategies showed remarkable growth in October. The standard Market Neutral strategy achieved a 91.14% win rate, while the Market Neutral Aggressive climbed to 93.43%, surpassing the 90% benchmark. These results reinforce their value as essential stabilizers within a diversified trading setup, providing consistent performance regardless of broader market direction.

Check out the performance data for the strategies below:

Scalping and short-term trading bots also registered meaningful improvements. Gamma MAX achieved a solid 80.25% win rate, benefitting from sharp intraday volatility, while Ultra Scalp MAX and Ultra Scalp held steady at 78.52% and 83.53%, respectively. These bots capitalized effectively on quick market reversals, demonstrating the benefit of having tactical intraday exposure within a balanced portfolio.

Conservative strategies continued to prove their worth. The Swing Strategy delivered a robust 94.21% win rate, while the Fishing Rod Strategy delivered a 90.39% win rate, giving users dependable options for steadier, lower-risk returns.

Users who maintained a balanced mix of large-cap and small-cap (or penny) stocks achieved better overall results than those who concentrated solely on one segment. While large-cap stocks tend to exhibit greater stability and resilience during market downturns, small-cap stocks typically outperform in bullish conditions due to their higher growth potential. Maintaining a well-diversified blend of both large- and small-cap exposures is therefore essential in building a risk-adjusted trading bot portfolio capable of performing across varying market environments.

The takeaway from October is clear: diversification and risk-balanced automation remain key to long-term trading success. As the Sigma Series Alpha’s performance illustrates, it’s not always the most aggressive strategies that win in volatile times. Instead, a well-structured mix of bots — from market-neutral to bullish and swing-focused — ensures traders are prepared to thrive, no matter how unpredictable markets become.